Stuck in a Starter Home

If buying a home is an inexorable part of the American dream, so is the next step: eventually selling that home and using the equity to trade up to something bigger.

But over the past two years, this upward mobility has stalled as buyers and sellers have been pummeled by three colliding forces: the highest borrowing rates in nearly two decades, a crippling shortage of inventory, and a surge in home prices to a median of $434,000, the highest on record, according to Redfin.

People who bought their starter home a few years ago are finding themselves frozen in place by what is known as the “rate-lock effect” — they bought when interest rates were historically low, and trading up would mean a doubling or tripling of their monthly interest payments.

Sign up for The Morning newsletter from the New York Times

They are locked in, and as a result, families hoping to buy their first homes are locked out.

“Home affordability is the worst I’ve ever seen it,” said Daryl Fairweather, Redfin’s chief economist.

A year ago, Chris and Alison Wentland were eager to sell their townhouse in the coveted Lincoln Park neighborhood of Chicago, so they hired a real estate agent who sent a photographer to take slick photos of the house, including a 3D video that panned from room to room.

The couple’s children — then ages 2 and 6 — shared a room barely big enough to fit a crib and a twin-size bed. A year later, the children share a bunk bed and the couple haven’t even listed the house, much less bought a new one. It’s not that they can’t find buyers; they just can’t afford to sell.

“If I had an open house this weekend, within seven days we’d have an offer, if not multiple offers,” said Chris Wentland, 38. “But the flip side to it is: What’s going to happen on the other end?”

The other end looks like this: Although they’ve been lucky enough to accrue equity thanks to rising home prices — the townhouse they bought a few years ago for $538,000 will likely fetch more than $700,000 now — the same wave that lifted their home’s value has pushed other homes in their neighborhood out of reach.

For an extra bedroom in Lincoln Park, they would need to spend at least $1 million. And it would mean getting a new mortgage, foregoing their 2.25% rate — close to the bottom of the historic curve — for one close to 7%, which is hovering near a 20-year high. Their monthly interest payments would triple to at least $7,500, their agent warned.

It’s a financial impasse that is repeating itself across the country. “The take-home message is that people are stuck,” said William M. Doerner, a supervisory economist at the Federal Housing Finance Agency.

“‘Stuck’ is a good way to put it,” Wentland said. “I don’t know what the right thing to do is, because there’s no obvious thing to do.”

Locked In

Currently, more than 6 out of every 10 U.S. homeowners have mortgages locked at rates that are extremely low — 4% or less, according to Freddie Mac.

Avoiding the new, higher rates has become a huge deterrent not just to buying but to selling, which in turn has reduced inventory for prospective buyers.

Last year, about 900,000 fewer homes changed hands than in a typical year, according to a research paper by economists at the Federal Housing Finance Agency. The result, according to the authors, “restricts mobility, results in people not living in homes they would prefer, inflates prices, and worsens affordability.”

“The starter home for many has become a keeper home, unfortunately,” said Susan M. Wachter, a real estate professor at the University of Pennsylvania’s Wharton School and a former assistant secretary at the Department of Housing and Urban Development.

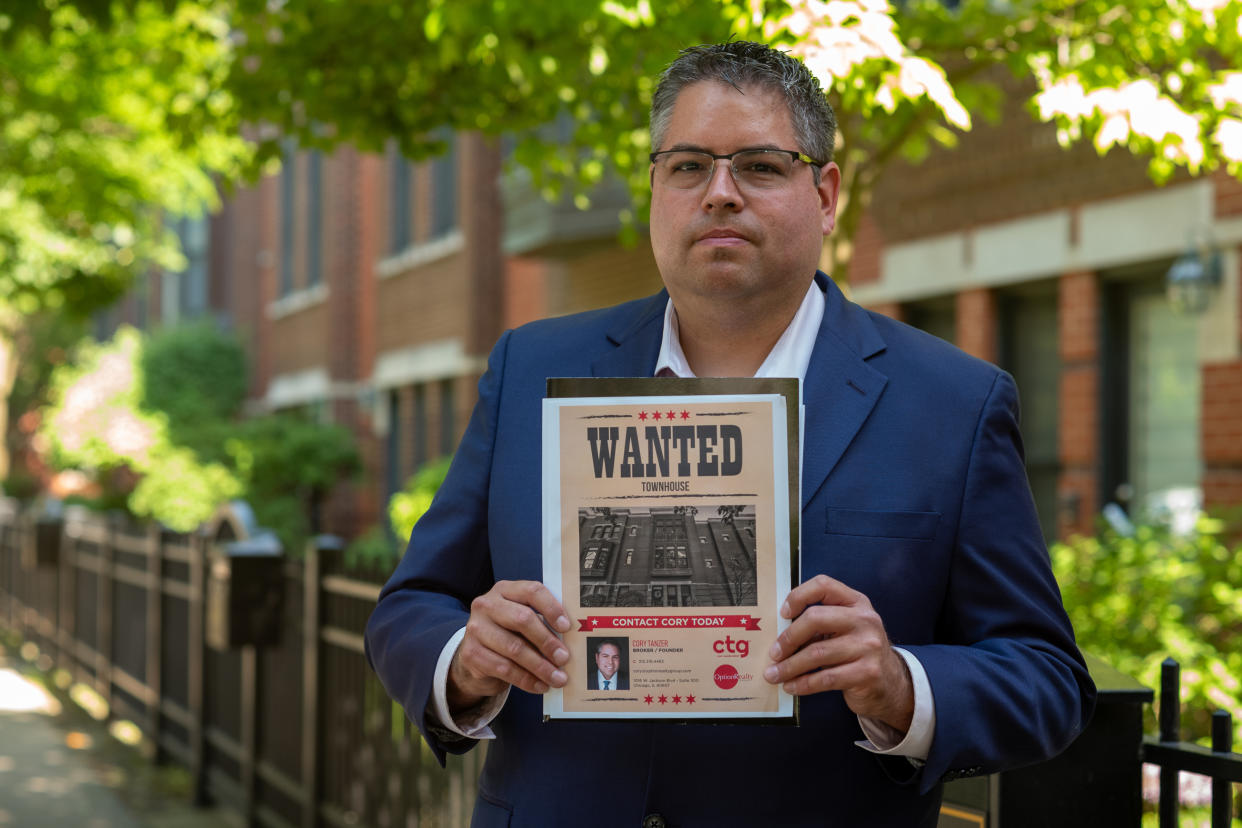

Cory Tanzer, the agent representing the Wentlands in Chicago, keeps a Dropbox folder with images of about 50 properties that have been professionally photographed. So far, his clients have been unable to list those properties for fear of not finding a trade-up home they can afford. Tanzer, who leads a team of brokers at the Option Realty Group, has taken to walking the streets of University Village, a neighborhood cater-cornered to the Chicago Loop, knocking on doors to see if anyone wants to sell their home.

To get a laugh, he carries with him an old-fashioned “Wanted” poster showing a mug shot of a townhouse.

Another couple that Tanzer represents, Kevin Ryan and Ella Yung, are stuck on the other side of the equation — they can’t afford to buy.

The couple, who have a 20-month-old, began with a budget of $700,000 and stretched it as far as they could, making offers on eight houses, sometimes bidding more than $800,000. Each time they were outbid, including for a home where they included an escalation clause indicating they were willing to spend $105,000 over the asking price.

“Every week we feel so downtrodden and, like, heartbroken over whatever house we lost recently,” said Ryan, 36. “Maybe this is just the cosmos telling us that it’s time to leave Chicago area.”

Their break finally came over the Memorial Day holiday, when most buyers were enjoying the beautiful weather. The couple found a house that hadn’t yet come to market and made an offer within 16 hours of learning about it — as of this writing, their ninth bid had been tentatively accepted.

Most people haven’t been as lucky.

Some 900 miles away in Virginia Beach, Virginia, Talia Phillips and her husband started looking for a trade-up home last summer, after their third child was born. Their daughters, ages 7 and 11, had their own rooms in the family’s three-bedroom house, while the couple shared the third with the baby.

A year later, they were optimistic about the equity they’d amassed in their starter home. But when they learned that their mortgage would jump from $1,300 a month to about $3,000 if they bought a new house, they called off their search. “I’m just a little frustrated, and hope that, you know, in a couple years, interest rates will go down,” Phillips said.

Those With Less Pay More

With buyers and sellers in higher price tiers effectively paralyzed, the weight of the housing market is pressing down hardest on those with the least to spend.

“The trade-up buyer has just disappeared,” said Sam Khater, chief economist at Freddie Mac, explaining that homeowners who are unable to upgrade are instead going down in the price continuum. “The lack of supply, it’s not just that it’s causing prices to go up, but it’s causing prices in the bottom half of the price distribution to go up even more.”

Prices in the lowest tranche of the housing economy are growing at a faster rate than in any other category. Over the past 20 years, the price for entry-level homes — defined as homes that cost 75% or less than the median in a given market — has nearly tripled since 2004, according to CoreLogic, a property information firm. (A starter home fitting this definition in Manhattan is as high as $863,000, while one in Cleveland is no more than $142,000, according to Alex Lacter, a spokesperson for Zillow.)

Every other tier of single-family homes has also increased — just more slowly. Overall, during the same period, the average price increase for single-family homes was 113%.

If those conditions weren’t tough enough, first-time buyers and people in their first homes are now competing against a wave of investors and all-cash buyers who can forgo the mortgage game — 28% of U.S. homes sold in April were bought entirely in cash, according to the National Association of Realtors.

In Virginia Beach, Yamilet Booker spent months feverishly sending inquiries to her broker on nearly 50 homes that fit her family’s needs, including a budget in the low $300,000 range. By the time her broker responded, the house she’d seen was already in contract. Meanwhile, the median sale price for a single-family home in Virginia Beach was growing from just over $300,000 at the start of 2020 to nearly $450,000 this April, according to Redfin.

After months of searching, Booker, 22, and her husband, Marquell Booker, made a series of compromises and closed on a $325,000 house not in Virginia Beach but in the cheaper city of Portsmouth, Virginia.

The house is on a busy, two-lane road, and Yamilet Booker worries about her toddler.

“We know that a lot of people our age aren’t able to buy homes, so we were grateful that we had the ability to buy one,” she said. “But at the same time, it was like, you know, for how much we’re making, we should be able to get something nicer. It’s just a very compromised feeling.”

The Housing Crunch

For decades, the U.S. has failed to build enough housing to keep up with demand — a problem that is widespread and affects all types of housing, but is especially pronounced for starter homes, economists say.

During the 1970s, more than 400,000 entry-level homes — defined as those that are no more than 1,400 square feet — were built in the United States each year, according to a report by Freddie Mac. In the 2000s, that number shriveled to about 150,000 a year. By 2020, just 65,000 starter homes were built. Yet 2.38 million people purchased their first homes that year, according to the report.

Among the reasons for the shortage is the price of building materials, which has shot up in the wake of the pandemic. The small margins that builders could expect to make on a smaller home just don’t pencil out, said Khater, the Freddie Mac economist.

Many people trying to buy their starter homes are finding only fixer-uppers.

“We can’t go buy something that is uninhabitable,” said Dania Anderson, 51, who pooled her resources with her sister, Tiffany King, in an effort to buy something in the pricey Bay Area.

They were approved for a combined mortgage of $850,000 before the pandemic and began their house hunt in Oakland, California. The plan was to buy a duplex, with each sister taking one unit. But the housing stock was so limited that everything in their budget had issues. One house they saw had a rat infestation. Another had fungus, and a third came with a ground-floor unit that was zoned as a business and had been illegally converted into an apartment.

As they waited, the housing market shifted beneath their feet. Their banker recently told them that they now only qualify for a $750,000 loan — $100,000 had evaporated as rates soared. Now the sisters wonder if they’ll be able to enter the housing market at all.

“I saved my money,” King said, “but I’m not getting what I want.”

c.2024 The New York Times Company