Semiconductors Update: More Pain or Time to Buy?

Advanced Micro Devices is a multinational semiconductor business based in Santa Clara, California that produces computer processors and graphics chips. AMD reported earnings Tuesday January 31 after the market closed.

AMD beat Q4 sales and earnings expectations, but project Q1 FY23 to experience a -10% YoY decrease in revenue.

Quarterly results from AMD significantly outperformed its peers, though it cited falling consumer PC demand as a headwind.

During the post Covid boom, semiconductor stocks like AMD, Texas Instrument TXN and Intel INTC led the market higher because of increased demand and supply chain related shortages. But since those peaks, they have led the market lower, and now with a supply gut in chips the pain may not be over. This is not new for microchips, as a commodity-like product the market regularly experiences cyclical ups and downs.

Earnings Review

2022 was a strong year for AMD, reporting record full year revenue of $24 billion, up 44% YoY. As was seen in the Microsoft MSFT earnings, and in Apple’s AAPL earnings expectations, demand for computers is falling, so it is commendable for AMD to have had such a successful year.

The near future looks challenging though. After the near parabolic rise in sales following Covid, it looks like sales peaked in Q2 FY22. Q4 sales were flat QoQ, and Q3 sales were down -15% from Q2. It is no surprise AMD management pointed out the weakness expected next quarter.

Revenue: $5.6 billion vs. $5.5 billion expected

Adjusted EPS: $0.69 vs. $0.67 expected

Data Center: $1.7 billion vs. $1.6 billion expected

Client: $903 million vs. $995 million expected

Gaming: $1.6 billion vs. $1.5 billion expected

Embedded: $1.4 billion vs. $1.3 billion expected

Image Source: Zacks Investment Research

Competitors

We can’t talk about semiconductors without bringing up Intel’s earnings report from last week. INTC’s Q4 revenue fell -32% to $14 billion and made just $0.10 per share in the quarter.

The CEO was hopeful on Intel’s earnings call, stating “In the fourth quarter, we took steps to right-size the organization… These actions underpin our cost-reduction targets of $3 billion in 2023, and set the stage to achieve $8 billion to $10 billion by the end of 2025.”

Clearly, Intel is making cuts, and the CEO announced on Wednesday he will be taking a 25% pay cut, while the executive team salaries will be cut 15%.

INTC’s CEO also said that customers are going to have to “digest” the current supply and that “While we know this dynamic will reverse, predicting when is difficult.”

Image Source: Zacks Investment Research

Chip Outlook

Most people remember just a year ago how challenging it was to buy a new car, or new computer parts because of the shortage of microchips. Well that dynamic has completely flipped as now there are more chips than the producers know what to do with.

With the rush that was 2020 and 2021, many were outfitting their new home offices, and spending some of their stock market gains on gadgets and cars. It seems that this demand was pulled forward a couple of years, and because they extrapolated forward that demand, they are now left holding a big bag of chips. Intel’s CEO went so far as to predict a million chips a day in 2021, but PC sales are closer to 270 million a year right now. It seems the industry got ahead of itself.

Valuation

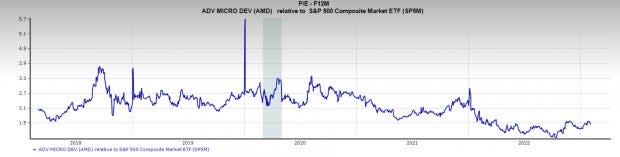

After an epic run followed by a challenging year, chip makers are anticipating some lean times, AMD included. But it isn’t all bad news. AMD is currently in the lower range of its historical forward P/E. With a forward P/E of 26x, it is well below its five-year median of 40x, and is already discounting bad news. Ideally stocks should bottom when the news is bad right?

Relatively speak, AMD also appears to be a better run company than INTC now. Valuations reflect that INTC currently has a one year forward P/E of 16x.

Image Source: Zacks Investment Research

Additionally, on the chart it seems AMD has found some technical support at the pre-Covid highs. Price holding above here would be a very promising development.

Image Source: Zacks Investment Research

Conclusion

Semiconductor manufacturing is a strong business model. Creating chips for technology that is growing exponentially and doing it at a 50% gross margin is a great place to be. Unfortunately, the industry is prone to cyclical returns, marked by booms and busts, and it appears that we are in the midst of that.

Can AMD stock price trade lower? Of course. Is it an extremely well positioned business for long-term success? A resounding yes.

Want the latest recommendations from Zacks Investment Research? Today, you can download 7 Best Stocks for the Next 30 Days. Click to get this free report

Intel Corporation (INTC) : Free Stock Analysis Report

Texas Instruments Incorporated (TXN) : Free Stock Analysis Report

Advanced Micro Devices, Inc. (AMD) : Free Stock Analysis Report