Philip Morris Earnings Preview: Smoke-Free Boosting Sales

Philip Morris International PM, reports earnings on Thursday, February 9 before the market opens.

The tobacco and smoke-free nicotine alternative company continues to transition towards a smoke-free product line, evident from the shifting revenue streams.

Transition

Smoke-free products now make up more than 30% of total Philip Morris revenue. The firm’s acquisition of a nicotine pouch company, Swedish Match continues to help grow Philip Morris’ smoke-free segment.

The strategic move from Philip Morris has some interesting implications. Expectations for sales growth and margins are suffering in the short-term, but with changing consumer sentiment towards smoking, its likely that Philip Morris is setting itself up for long-term success. Furthermore, it makes the stock more compelling to investors, many of whom have opted out of investing in tobacco companies because of health concerns.

But while vapes and other smoke-free options appear to be an improvement in regards to consumers health, the long-term effect of the products are still somewhat unclear. Nonetheless, PM is committed to the plan.

Earnings Expectations

Philip Morris Q4 sales and earnings are expected to see a decline according to Zack’s estimates. Q4 sales are projected for a YoY decline of -8.2%, bringing sales down to $7.4 billion. Earnings are expected to come in at $1.29 per share, a -4.4% YoY decrease. However, PM still earns a Zacks Rank #1 (Strong Buy), because of its positive earnings revisions trend.

Analysts have mixed projections for current quarter earnings, with seven analysts revising higher over the last 60 days, and four revising lower over the same period. But next year’s earnings have analysts in unanimous agreement, with all eleven analysts revising expectations higher over the last 60 days. FY23 EPS has been revised from $5.60 per share to $5.96 over the last 90 days.

Image Source: Zacks Investment Research

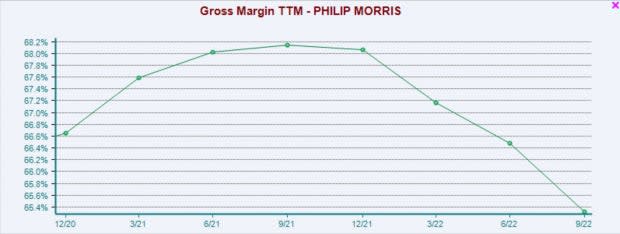

Smoke-Free

Philip Morris’ business transformation hasn’t happened without some risks and challenges. Since Q4 FY21, margins have compressed by nearly 300 bps. However, PM is betting that this will pay off in the long-term as consumer habits change to prefer smokeless options.

Image Source: Zacks Investment Research

Philip Morris isn’t stopping with vapes either. At the end of 2022, PM became the sole owner of Swedish Match, the leading nicotine pouch product in the world. I know personally, I have seen an explosion in the use of their product Zyn. The acquisition cost PM $16 billion, and makes for a significant new additions to their product line.

An added benefit of PM’s acquisition of Swedish Match, is that it brings them back into the US market for the first time in 14 years. This move should keep PM’s US competitor Altria MO on its toes.

Philip Morris has big plans as a smokeless company and states, “By 2025, our target is to increase that figure to at least 50 percent, with the ultimate goal of phasing out cigarettes completely. We also aim for USD 1 billion in annual net revenues to come from wellness and healthcare products.”

Valuation

Philip Morris currently trades at a one year forward P/E of 16.9x, a premium to the industry average, and just above it’s 5-year median of 15.2x. With the ongoing transition the company is going through it is quite impressive that it can maintain a premium valuation. That may signal investors giving PM a vote of confidence.

Image Source: Zacks Investment Research

PM is not a high-flying growth stock, but it is definitely a steady earner. The stock also has a very appealing 5% dividend yield.

Image Source: Zacks Investment Research

Conclusion

If you are an investor willing to stomach an allocation to a tobacco company, Philip Morris may well be a great addition to your portfolio. PM is actively shifting its business to be well positioned for the future, has a long history of success and offers the stability of a generous dividend yield.

Want the latest recommendations from Zacks Investment Research? Today, you can download 7 Best Stocks for the Next 30 Days. Click to get this free report

Altria Group, Inc. (MO) : Free Stock Analysis Report

Philip Morris International Inc. (PM) : Free Stock Analysis Report