Is Home Country Bias Bad in Investing?

Home country bias happens when investors are over-exposed to domestic equities in their investment portfolio. Let’s look at how it happens, and what the pros, cons and worst-case scenarios are when having this bias inherent in your portfolio.

How Does Home Country Bias Happen?

Looking back at the history books, before the arrival of the internet, investors sometimes had a lack of information about companies outside of their home jurisdiction. As such, it would be natural for a conservative investor to buy companies or securities that they had the most information about, which leads to an over-exposure to domestic equities.

Fast forward 20 or 30 years and the opposite is now true. Investors today arguably have an overabundance of information, yet the effect is somehow the same. Investors still often mostly consume information that pertains largely to their local market, again resulting in an unjustified comfort in investing locally.

It can also be argued that there is a certain emotional connection to investing in domestic companies. As we go about our day-to-day lives, seeing and touching the result of our investments can add a layer of comfort or even pride. Remember though that pride by itself won’t get you to retirement.

The Good

Avoiding Currency Risk

Wherever you live, you will need to spend local currency. When investing in companies internationally, you will first need to convert your local currency to that of the market where you are investing. When you sell your security, you once again need to convert that currency back into your local currency so that you can spend it. Between these two times, the foreign exchange rate will likely fluctuate. Moreover, the change of that rate will be independent of the price of the security that you purchased, meaning that even though your stock gained in value, you may end up losing on the trade due to foreign exchange translation. This added dimension is called currency risk and can work for or against you.

Possible Tax Advantages

Some jurisdictions offer tax benefits to investors who keep their assets within the country. This is particularly relevant for dividend investors since dividend income can be taxed differently depending on whether the company issuing the dividend is listed domestically or internationally. A quick internet search or a look at the recent Morningstar Global Investor Experience on Taxation and Regulation can provide insights into the tax rules in your local market.

Globalisation and Market Correlations

Over the year, economies have become increasingly globalised and connected. As a result, the correlations between major stock markets have also increased - something we've seen during the Covid-19 pandemic and 2008 financial crisis. In extreme market situations like these, correlations increase sharply which can negate the effects of geographical diversification at least over short time frames. The below chart highlights this idea by illustrating the trailing six-month correlation of various Morningstar country indices to the Morningstar US Market index. In other words, it illustrates the extent to which various country’s equity indices move in tandem with the US index.

Although not the case for every country, we can see that correlation between several major developed countries has increased against the US market particularly over the last five years. From this angle, diversifying globally (depending on the country) may not give the benefits that it did ten years ago.

Moreover, as international mega-cap companies continue to emerge, we can see that these large companies themselves are diversifying their revenue streams across regions and passing that benefit to investors directly. That said, not all investors have a large multi-national company listed in local markets.

The Bad

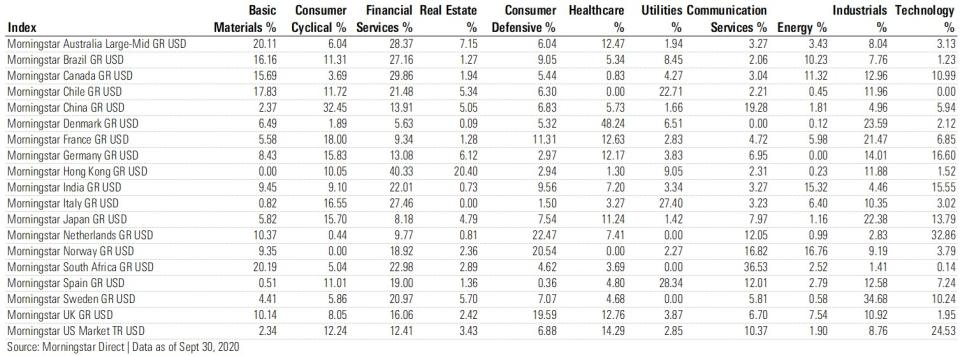

Diversification Across Sectors

Depending on the size of your local market, not every part of the increasingly connected global economy may be represented by a set of quality publicly-traded companies. Morningstar and others define 11 sectors illustrated in the table below along with the sector exposure of select country indices.

For example, if you live in the UK or South Africa, the chances of you being able to invest locally in a quality technology company are slimmer when compared to the US. The issue here is two-fold (1) if you restrict yourself to local markets, you may fail to uncover opportunities in sectors that are outperforming (technology, for example in recent past) and (2) investing only in local markets does not in all cases allow you to diversify fully across the economy. As an example, Canadian equities have recently underperformed due to the large exposure to energy and lower oil prices.

Don’t Just Take our Word for it

If you are lucky enough to be in a country that has a mandated retirement pension contribution system, it is likely that a large public pension fund is managing a portion of your retirement assets. If you have a look at the holdings of your local state-run pension fund, it is highly likely that the exposure to domestic securities in that portfolio is much lower than your own. Public pensions understand well the benefits of diversification and what’s more, de-risking by reducing exposure to the very economy that they are managing a pension for (more on this in the next section).

The Ugly

The Double-Whammy

In terms of human capital (i.e. our ability to work and make money) and financial capital (i.e. the assets we have and invest), it makes little sense for a conservative investor to put 100% of both in the same geographic region.

As much as the world is increasingly connected, the broad majority of us are still impacted heavily by our local economies since we are often employed by local companies or potentially satellite offices of global corporations. Along these lines, it is arguable that we have less control over where we invest our human capital. However, we do have control over where we invest our financial capital.

When both human capital and financial capital are invested in the same market, we expose ourselves to a potential ‘double-whammy’, which is the worst-case-scenario when we simultaneously lose our job due to poor economic conditions (crippling our human capital) only to see that our portfolio value also suffers for the same reason (reducing our financial capital). Ideally, investors can lessen this effect by ensuring that all eggs are not in the same basket, i.e. reducing exposure to domestic markets.