Freelancer’s Guide to Securing a Home Loan in Singapore: 6 Things to Look out For (2023)

How many freelancers are there in Singapore? Well, according to the Comprehensive Labour Force Survey 2022 conducted by the Ministry of Manpower, there are 257,300 residents in Singapore who engaged in “own account work”. What this means is freelancers account for 8.3% of all employed residents in 2022.

Unfortunately, for most freelancers, home ownership is a tricky task to navigate. Home loans tend to be more favourably geared toward employed individuals who earn a regular, salaried income.

However, if you intend to take up freelancing as a long-term occupation, there are several things you should take note of before applying for a home loan. Here’s a quick guide on what are the criteria affecting your ability to take on and be approved for a mortgage.

Table of contents:

Factors affecting mortgage eligibility and the amount you can borrow

As a freelancer buying an HDB flat, should you choose a bank or HDB loan?

1. Income

30% Haircut on All Variable Income

Banks apply the same ‘rules’ for salaried and self-employed people, in that all variable income will receive a 30% haircut. The difference is that for most salaried workers, only a small part of their income is variable, so it’s not as significant. For freelancers, your entire salary is likely variable.

Does Income Stability Matter?

Clearly, income is the first thing that any bank will take into consideration when anyone applies for a personal home loan. As a freelance, your first concern may be around income stability.

Your income stability matters to some extent! Banks are in the business of looking at your ability to service the loan on a monthly basis. To assess your income stability, they look at your IRAS Income Tax Notice of Assessment (NOA) over a period of two years, not so much that you earn the exact same amount every month.

Increase Your Income As Much As Possible Before Applying

In an ideal situation, you would want to increase your income as much as possible before you apply for a loan. That’s because how much you earn will affect your TDSR, which directly affects the loan amount you can borrow.

You want to ensure that before you embark on applying for a loan, you are in the best possible place to get one. If it has been a bad year for you financially (no thanks to the COVID-19 pandemic), we suggest making sure that your earnings are back up for at least two years before you apply for a home loan (although most banks look at one year).

As banks look at your IRAS Income Tax Notice of Assessment (NOA) and a 30% haircut is already taken on the variable income, banks don’t necessarily look at how ‘stable’ your income is, or the exact consistency between months.

2. TDSR

Your TDSR Affects How Much Loan You Can Get

Say you earn a total of $5,000 a month on your freelancer income. Since this is considered variable income, you will have to take a 30% haircut; in other words, the bank will only consider 70% of your declared income as a basis for a loan offer.

This means the amount of money a bank will offer to loan you will be based on a $3,500 income, which significantly reduces how much you can borrow. And that’s why it’s also important to correctly declare your income!

As most banks do not allow for your Total Debt Servicing Ratio (TDSR) to exceed 55% of your income, that means your monthly mortgage repayments cannot exceed $1,925 every month. This assumes you have no other financial commitments except paying for your house.

3. Credit Score

When it comes to taking a bank loan, banks will look at your credit score. Your credit score is a gauge of your ability to repay the debt.

If you have a good credit score, you will be deemed as a ‘safe bet’ for banks that you will pay back your mortgage payments. Banks are more likely to extend you a loan with favourable terms if you are able to make timely payments on your credit.

Conversely, late payments will affect the loan that a bank is willing to give you as well as the loan tenure you get. Check your credit score to know where you stand on this. And if you have a poor credit score, check out some tips to improve your credit score.

4. CPF OA Contributions

Speaking of CPF contribution charges, most people opt to use their CPF Ordinary Account (CPF OA) to foot the downpayment for their property, whether fully or in part. Additionally, you can use your CPF OA monies to pay your monthly mortgage payments and for conveyancing fees.

As such, if you can afford it, you may consider topping up your CPF OA before applying for a mortgage. Having sufficient funds would mean that you won’t have to worry as much about how to finance your property purchase. The only thing you have to take note of is how it may affect your CPF withdrawal limits.

Do note: Any amount used from your CPF OA account for the mortgage will need to be refunded back to CPF OA with accrued interest upon the sale of your property.

5. Paperwork and Tax Returns

You want to be diligent with declaring your income, tracking invoices and tax statements, and contributing to your Medisave, CPF OA accounts. The idea is to keep your accounts in order: you want to have receipts to prove your income.

For those who are setting up a company or are freelancers, your business needs to be in existence for two years before the bank can recognise your self-employed income. Generally, you should ensure that your tax returns for the last two years provide a full and pleasant picture of your ability to earn income for yourself.

If your computerised slips and bank statements do not provide a full enough picture, at the very least, this will be able to keep your accounts in check and establish a stronger picture with your bank of choice.

Financing Your HDB Flat As A Freelancer: Bank Loan vs HDB Loan

If you’re a freelancer who is buying a private property, you can only finance your property with a bank loan. But what if you’re buying an HDB flat: should you go for a bank loan or an HDB loan?

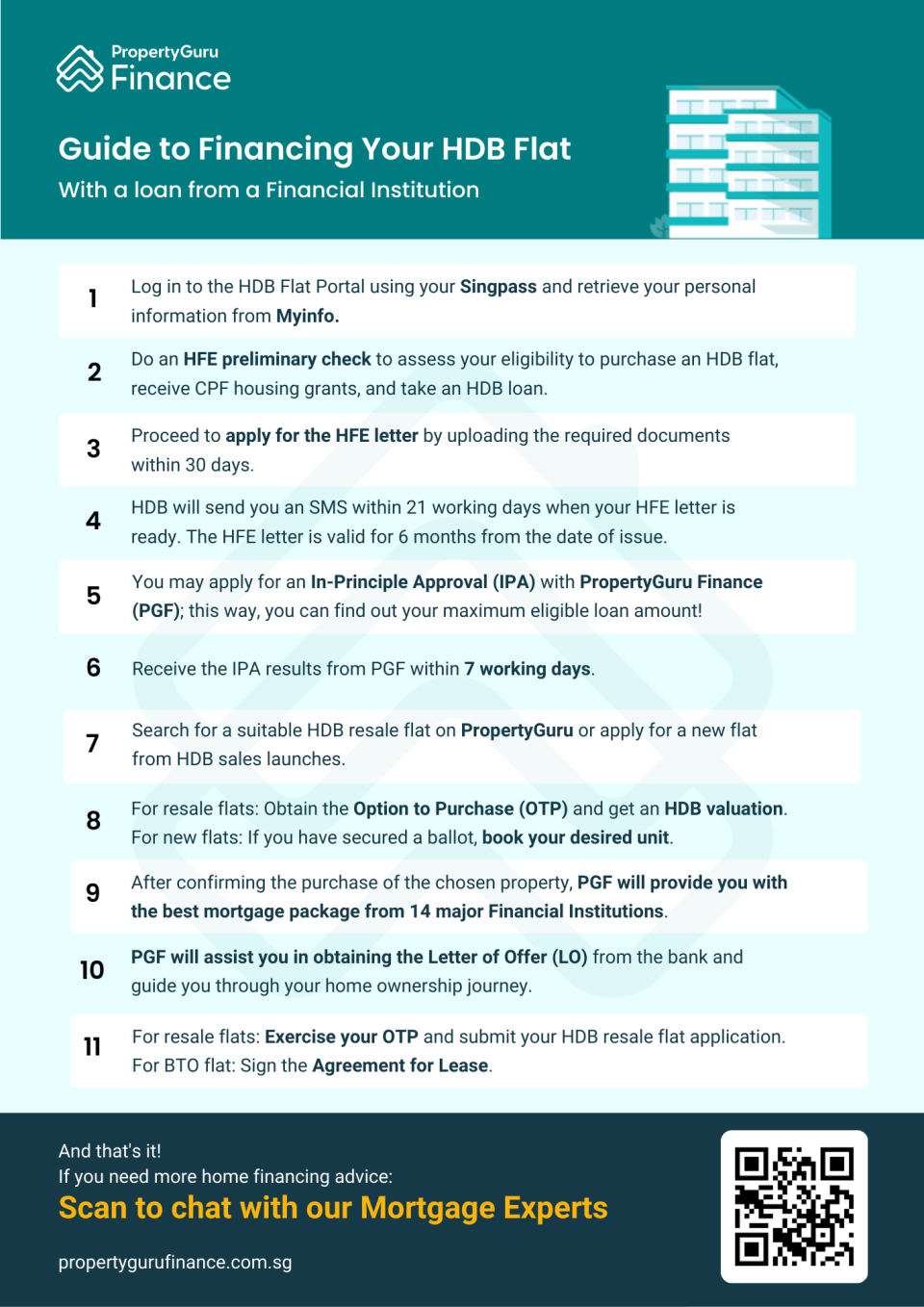

For those purchasing an HDB flat, you would have to apply for the new HDB Flat Eligibility (HFE) letter through the HDB Flat Portal. Taking effect from 9 May 2023, the HFE letter will inform you of your HDB flat eligibility, CPF Housing Grant eligibility and the amount you qualify for, and HDB loan eligibility and the amount you can loan.

Through the HDB Flat Portal, you can also request an In-Principle Approval (IPA) and Letter of Offer (LO) from participating Financial Institutions (FIs). Additionally, you can review potential loan options from said FIs. Here’s a quick guide on what the buying timeline would look like.

However, Paul Wee, Vice President – PropertyGuru Finance mentions that “homebuyers with special circumstances, such as those who earn an irregular income, or those who receive dividends, may not receive the most thorough assessment” when submitting their HFE application.

“As compared to salaried workers, freelancers have unique financial situations due to their variable income. For instance, despite a freelancer’s variable income, their income is considered to be ‘fixed’ at the point of application. So, if you do earn more after submitting your HFE letter, you may not be able to secure a better home loan package.”

“So what can you do? Speaking with a Mortgage Expert who is well-versed with the ins and outs of the home loan application process can provide critical, objective advice.”

Choosing the Best Home Loan for You

Generally, the eligibility criteria for freelancers are slightly different from salaried employees. While everybody – freelancers and salaried employees – enjoys the same interest rates, your income and tax documents can affect the rates and loan amounts that the bank will offer you.

If you need guidance, PropertyGuru Finance’s Home Mortgage Experts will be able to accurately advise you on the loan for your dream home. They can give you tailored, financial advice, ensure that your finances are in good shape, and all your paperwork is in order before you embark on your home ownership journey.

With this article, hopefully, you will be ensured that your choice to enter the gig community would not be one that you regret when it comes to buying your own home!

Chat with us on Whatsapp Fill up an online form

Disclaimer: Information provided on this website is general in nature and does not constitute financial advice.

PropertyGuru will endeavour to update the website as needed. However, information can change without notice and we do not guarantee the accuracy of the information on the website, including information provided by third parties, at any particular time. Whilst every effort has been made to ensure that the information provided is accurate, individuals must not rely on this information to make a financial or investment decision. Before making any decision, we recommend you consult a financial planner or your bank to take into account your particular financial situation and individual needs. PropertyGuru does not give any warranty as to the accuracy, reliability or completeness of information which is contained on this website. Except insofar as any liability under statute cannot be excluded, PropertyGuru and its employees do not accept any liability for any error or omission on this website or for any resulting loss or damage suffered by the recipient or any other person.