DCP Midstream (DCP) Units Rise 6.5% Since Q1 Earnings Miss

DCP Midstream, LP’s DCP units have increased 6.5% since May 5, despite lower-than-expected quarterly earnings. Investors are likely impressed by the fact that even though the partnership faced several negative impacts in the first quarter, it kept its 2021 financial guidance unchanged.

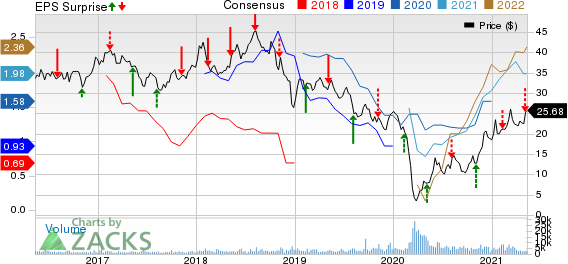

DCP Midstream reported first-quarter 2021 adjusted earnings of 19 cents per unit, missing the Zacks Consensus Estimate of 30 cents. In the year-earlier quarter, the midstream energy player incurred a loss of $2.71 per unit.

Revenues of $2,318 million beat the Zacks Consensus Estimate of $2,003 million. Moreover, the figure increased from $1,657 million in the year-ago quarter.

The partnership’s lower-than-expected quarterly earnings were caused by higher operating costs and expenses along with lower NGL pipelines volumes. The negatives were partially offset by higher natural gas storage and a favorable commodity environment.

DCP Midstream Partners, LP Price, Consensus and EPS Surprise

DCP Midstream Partners, LP price-consensus-eps-surprise-chart | DCP Midstream Partners, LP Quote

Operations

Logistics and Marketing

The segment recorded operating income of $146 million for the first quarter, down from the year-ago period’s $236 million. Lower NGL pipelines throughput volumes, caused by the winter storm Uri, affected the segment. The negatives were partially offset by higher natural gas storage.

Average NGL pipelines throughput for the quarter was 578 thousand barrels per day (Mbpd), lower than the year-ago level of 677 Mbpd. Fractionator throughput, moreover, decreased to 43 Mbpd from the year-ago level of 58 Mbpd.

Gathering and Processing

The segment reported net income of $27 million for the first quarter against a loss of $645 million a year ago. Decreased operating costs boosted the segment, partially offset by a decline in volumes.

Average wellhead volumes for the quarter declined to 4,077 million cubic feet per day (MMcf/d) from the year-ago period’s 4,940 MMcf/d. Moreover, NGL gross production decreased to 361 Mbpd from 404 Mbpd in the year-ago quarter.

Total Expenses

Purchases and related costs significantly increased year over year for the quarter under review. This was partially offset by decreased general and administrative expenses as well as operating and maintenance costs.

Total operating costs and expenses for the first quarter were $2,315 million, up from the year-ago figure of $2,203 million.

Financials

For first-quarter 2021, total expansion capital expenditure and equity investments were $4 million. Sustaining capital for the quarter was $10 million. It generated excess free cash flow of $89 million in the first quarter.

At the end of first-quarter 2021, the partnership reported long-term debt of $5,178 million, up from $5,119 million at fourth quarter-end. Cash and cash equivalents declined to $5 million from $52 million at fourth quarter-end. Moreover, it had current debt of $504 million.

View

The partnership kept its 2021 financial guidance unchanged.

Throughout 2021, it is expected to maintain stable distribution at $1.56 per unit on an annualized basis. Due to the coronavirus pandemic, DCP Midstream is expected to take a conservative approach through 2021 in regard to volumes and pricing of commodities. The partnership expects adjusted EBITDA for 2021 in the range of $1,120-$1,260 million, the midpoint of which is below the 2020 level of $1,252 million. It expects excess free cash flow to rise more than 60% in 2021 to $310-$460 million from the 2020 level of $237 million.

DCP Midstream expects expansion capital expenditures and equity investments within $25-$75 million in 2021, indicating a significant decline from $205 million in 2020. Sustaining capital expenditures for 2021 are estimated within $45-$85 million. The metric was $45 million in 2020.

NGL pipeline volumes are expected to rise this year supported by higher ethane recovery. However, overall profits might get affected by decreasing Guadalupe earnings. Also, Gathering and Processing volumes are expected to decline in 2021.

Zacks Rank & Stocks to Consider

The partnership currently has a Zacks Rank #3 (Hold). Some better-ranked players in the energy space include ConocoPhillips COP, NOW Inc. DNOW and PHX Minerals Inc. PHX, each having a Zacks Rank #2 (Buy). You can see the complete list of today’s Zacks #1 Rank (Strong Buy) stocks here.

ConocoPhillips’s sales figure for 2021 is expected to rise 92.2% year over year.

NOW’s bottom line for 2021 is expected to rise 86.2% year over year.

PHX Minerals’ bottom line for 2021 is expected to surge 40% year over year.

Zacks Top 10 Stocks for 2021

In addition to the stocks discussed above, would you like to know about our 10 best buy-and-hold tickers for the entirety of 2021?

Last year's 2020Zacks Top 10 Stocks portfolio returned gains as high as +386.8%. Now a brand-new portfolio has been handpicked from over 4,000 companies covered by the Zacks Rank. Don’t miss your chance to get in on these long-term buys.

AccessZacks Top 10 Stocks for 2021 today >>

Want the latest recommendations from Zacks Investment Research? Today, you can download 7 Best Stocks for the Next 30 Days. Click to get this free report

ConocoPhillips (COP) : Free Stock Analysis Report

NOW Inc. (DNOW) : Free Stock Analysis Report

DCP Midstream Partners, LP (DCP) : Free Stock Analysis Report

PHX Minerals Inc. (PHX) : Free Stock Analysis Report

To read this article on Zacks.com click here.

Zacks Investment Research