Crypto for Advisors: Is Crypto Too Volatile?

Today’s newsletter marks my one-year anniversary of curating the Crypto for Advisor newsletter. Time flies when you are having fun, and it’s hard to believe I have 52 issues under my belt. Thanks to CoinDesk and particularly Kim Klemballa for giving me this opportunity along with all of our valued newsletter contributors who spend their time building this industry as your contributions are invaluable. As we continue our crypto journey together, I hope to see new contributors and continued engagement with ideas and topics as we strive to deliver advisor education globally. Your educational needs, views and opinions are what shape this newsletter - as it is truly Crypto for advisors!

We understand the last couple of years have been challenging in the crypto space, but 2024 has brought excitement and energy back. We are seeing many exciting product launches and regulatory advancements. I look forward to continuing to provide content to our valued audience and to keeping them informed of timely and relevant developments.

In today’s issue, André Dragosch, head of research at ETC Group, discusses the volatility of crypto assets, including bitcoin and ether and how they compare to other emerging technology investments. Bryan Courchesne, CEO of DAIM, explains how advisors can navigate the volatility of crypto within client portfolios.

Happy Independence Day to our American readers.

– Sarah Morton

You’re reading Crypto for Advisors, CoinDesk’s weekly newsletter that unpacks digital assets for financial advisors. Subscribe here to get it every Thursday.

Are Crypto Assets Too Volatile?

Traditional financial investors tend to shun crypto assets because of the high volatility.

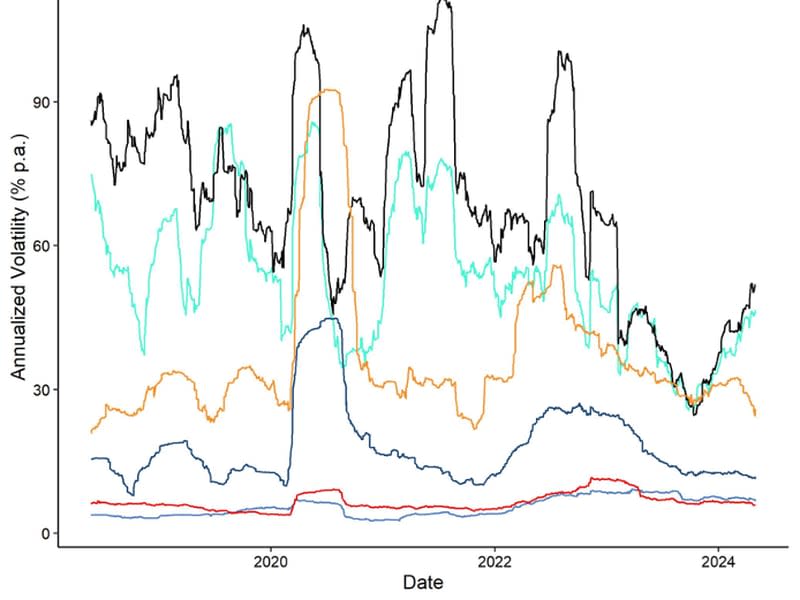

To be fair, the volatility of crypto assets is relatively high compared to traditional asset classes such as equities, bonds and most commodities.

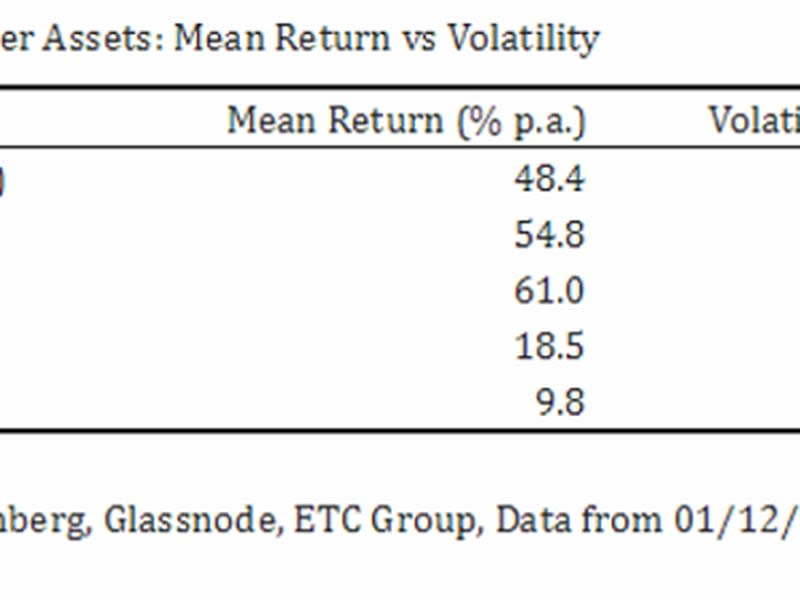

Over the past three months, the annualized volatility of bitcoin and ether has been around 45% to 50%, respectively, while the volatility of the S&P 500 was around 15%.

A recent survey by Fidelity among institutional investors also identified high volatility as the No. 1 most-cited barrier keeping investors from allocating to crypto assets.

However, the truth is that high returns come with high risks, i.e. volatility.

Put differently, where there is growth, there is volatility.

Most equity investors know this since most high-growth mega-cap stocks like Tesla still tend to have high double-digit volatility.

Will tokenization of real-world assets (RWAs) take off, and will Ethereum be the go-to platform?

Will bitcoin replace the U.S. Dollar as a global reserve currency?

Although these types of scenarios have become increasingly likely over the past few years, there remains uncertainty around these questions.

Uncertainty tends to create volatility.

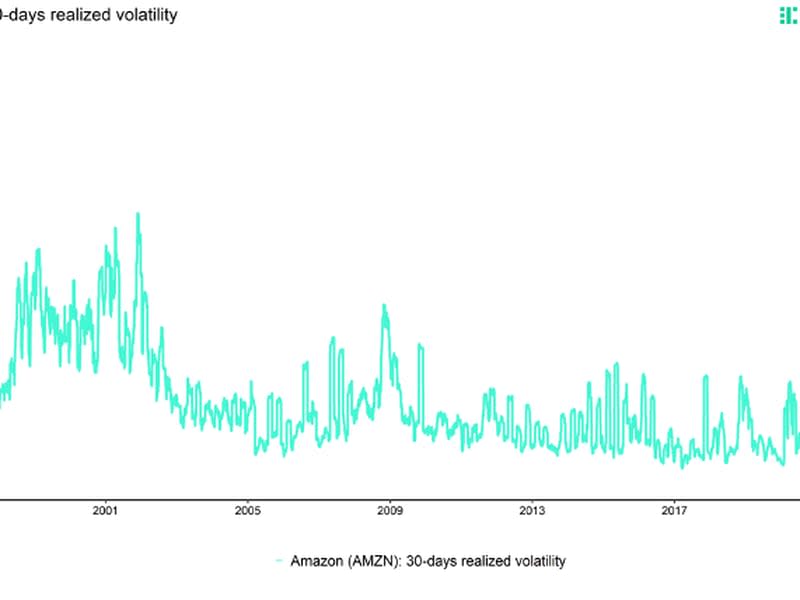

The history of Amazon holds important lessons in this regard. In the late 1990s, most Wall Street analysts thought “selling books online” was a silly idea. There was a lot of uncertainty about whether online retailing and the internet in general would eventually become mainstream.

In the same way that the uncertainty around the technology has declined, the volatility in Amazon’s stock price has declined over time.

Few investors seem to remember that Amazon’s stock used to record above 300% in annualized volatility in the late 1990s; today, the volatility is well below 50%.

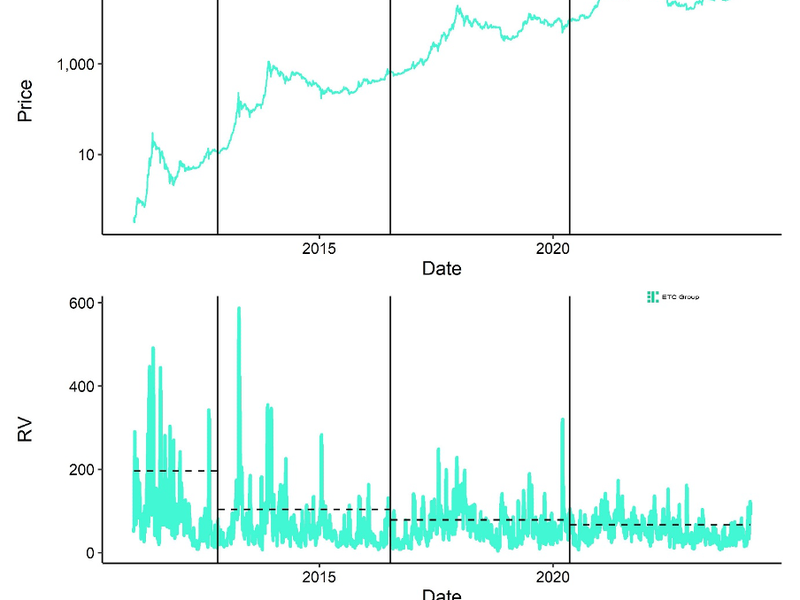

We have already observed a similar structural decline in volatility in the case of crypto assets.

One reason is that bitcoin’s scarcity has increased with every halving, making it more “gold-like.” Halvings are best understood as a supply shock that reduces the supply growth of bitcoins by half (-50%). Hence, the character of bitcoin as an asset class has changed over time

While bitcoin’s volatility was around 200% during the first epoch – the roughly four-year timespan between the cryptocurrency's pre-programmed "halvings" of miner rewards – until 2012, it has decreased to only 45% more recently. Similar observations can be made regarding ether.

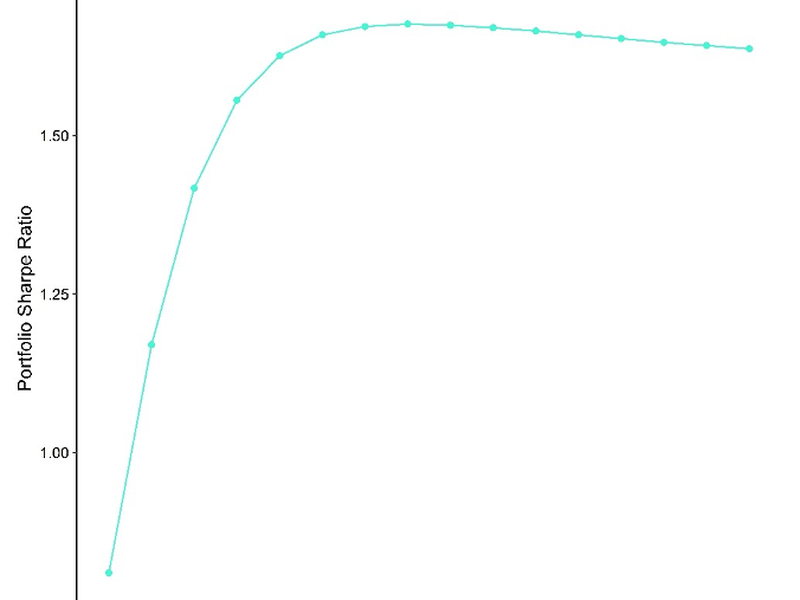

In a global 60/40 stock-bond portfolio, the maximum Sharpe Ratio is achieved by increasing the bitcoin allocation to around 14% at the expense of the global equity weighting.

The Sharpe Ratio of major crypto assets like bitcoin or ether is significantly above 1, which means that investors are more than compensated for exposing themselves to higher volatility.

Looking ahead, the decline in volatility is bound to continue with every new halving. The next one is scheduled to happen in 2028.

Increasing retail and institutional adoption of this technology is also bound to decrease volatility structurally over time.

The reason is that increasing heterogeneity among investors will lead to more dissent between buyers and sellers, which dampens volatility – the essence of Edgar Peters's Fractal Market Hypothesis.

Just remember: Where there is growth, there is volatility.

- André Dragosch, head of research, ETC Group

Ask an Expert

Q. How can advisors help their clients navigate crypto volatility?

A. Crypto, in its short history, has undoubtedly been a volatile asset. But that does not mean that it should be ignored by advisors. Advisors should not consider assets in isolation but rather how they interact with others in a well-balanced portfolio. When creating a portfolio that can deliver long-term results, diversification is key. Asset prices move in cycles, sometimes together but more or less distinct. This can be measured by an asset’s correlation to other assets. A lower correlation means assets are less likely to move together. If one asset is up 35% in the year, another asset might only be up 4%. If assets are negatively correlated, one asset will be up in a given period while the other will be down. This is important in the context of an investment portfolio because while assets may be volatile themselves, including them with other less correlated assets can lower the overall volatility of a portfolio.

Q. Is there a correlation between crypto’s volatility and other assets?

A. With respect to correlation, a volatile asset like crypto is actually very important to decrease the overall volatility of a portfolio. Lowering the overall volatility of a portfolio is important as it helps smooth investment returns over time. This is important for many reasons. For example, an investor could have significant and unpredictable liquidity needs. If they have a portfolio of highly correlated assets and those assets are experiencing a period of poor returns, they would be withdrawing a larger percentage of their portfolio compared to a portfolio that included less correlated assets. Crypto, having a low correlation with traditional assets, could help in this regard. Its volatility has historically been positively skewed so even though it has big swings, when all other assets are down it can provide a ballast to your portfolio. Smoothing returns also helps from a cognitive perspective for most investors. People can get too emotional when looking at their portfolio’s performance. Big price moves have a visceral effect where large moves up make people want to buy more (usually right before a drop) and large moves down make people discouraged and pull money out (right before performance rebounds). Including at least a small portion of (less-correlated) crypto in a portfolio smooths the returns of a portfolio so when investors check in, they see more modest gains or losses. This helps keep their portfolio out of sight and out of mind which generally improves the chances of long-term success. Crypto, while volatile, should not be viewed in isolation but in the context of how it can help create a truly diversified portfolio that will help create long-term wealth for investors.

Keep Reading

Revised spot Ether ETF date: the U.S. SEC has requested issuers submit revised filings by July 8.

Will Solana ETFs be available next? On June 28, 21Shares filed an S-1 application with the U.S. SEC for a spot Solana (ETF).

Bitcoin ETFs saw the largest inflows since June 7, with Fidelity leading at $65 million.

Note: The views expressed in this column are those of the author and do not necessarily reflect those of CoinDesk, Inc. or its owners and affiliates.