Buy These 4 High-Flying Tech Stocks That Can Rally Further

Making a remarkable rally in 2023, tech stocks have shown no signs of slowing this year. Improving earnings, along with the accelerating potential of artificial intelligence, seem to have subsided investors’ worries about challenges posed by macroeconomic headwinds, including still-high interest rates, protracted inflationary conditions and ongoing wars across several parts of the world.

With a year-to-date (YTD) rise of 14.4%, the tech-laden Nasdaq Composite has outperformed The Dow Jones Industrial Average and the S&P 500 index’s increase of 3.2% and 12.2%, respectively. Technology stocks have more than 50% of weightage in the Nasdaq Composite index. Technology Select Sector SPDR, the most important component of the broad market index, has returned 11.8% YTD.

Considering tech stocks’ resilience amid current macroeconomic uncertainties, it is wise to invest in the sector. However, investors should be careful in selecting stocks and look for fundamentally strong technology stocks that have sustained the market jitters so far and have the potential to carry the momentum further.

Here, the Zacks Stock Screener comes in handy. With the help of this Zacks tool, we have narrowed our search to four tech companies — NVIDIA Corporation NVDA, Dell Technologies Inc. DELL, Alphabet Inc. GOOGL and Micron Technology, Inc. MU — that have outpaced the gains of broader market indexes. Year to date, NVDA, DELL, GOOGL and MU stocks have surged 143.7%, 75.2%, 26.6% and 52.7%, respectively.

Moreover, these stocks have a favorable combination of a Growth Score of A or B and a Zacks Rank #1 (Strong Buy) or #2 (Buy). The Growth Style Score condenses all the essential metrics from a company’s financial statements to get a true sense of the quality and sustainability of its growth. Additionally, per Zacks’ proprietary methodology, stocks with a combination of a Zacks Rank #1 or #2 and a Growth Score of A or B offer solid investment opportunities.

Our Picks

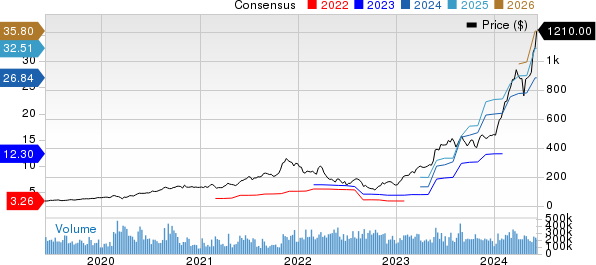

NVIDIA is the worldwide leader in visual computing technologies and the inventor of the graphic processing unit or GPU. Over the years, the company’s focus has evolved from PC graphics to AI-based solutions that now support high-performance computing (HPC), gaming and virtual reality (VR) platforms. The stock currently sports a Zacks Rank #1 and has a Growth Score of A. You can see the complete list of today's Zacks #1 Rank stocks here.

The company is gaining from the strong growth of AI, HPC and accelerated computing, which is boosting its Compute & Networking revenues. Its data center end-market business is benefiting from the growing demand for generative AI and large language models using GPUs based on NVIDIA Hopper and Ampere architectures.

A surge in Hyperscale demand and a solid uptake of AI-based smart cockpit infotainment solutions are acting as tailwinds for NVDA. The collaboration with several automobile companies is likely to advance NVIDIA’s presence in the autonomous vehicle and other automotive electronic space.

The Zacks Consensus Estimate for fiscal 2025 earnings has been revised upward by 11.6% in the past 30 days to $26.84 per share, which calls for an increase of 107.1% on a year-over-year basis. The long-term expected earnings growth rate for the stock is pegged at 36.7%.

NVIDIA Corporation Price and Consensus

NVIDIA Corporation price-consensus-chart | NVIDIA Corporation Quote

Dell Technologies is benefiting from the strong demand for AI servers driven by ongoing digital transformation and heightened interest in generative AI applications. Its PowerEdge XE9680L AI-optimized server is very much in demand. Strong enterprise demand for AI-optimized servers is aiding Dell Technologies.

It is witnessing demand from a diversified customer base that includes the likes of higher education institutions, financial services, health care and life services and manufacturing. An expanding partner base that includes the likes of NVIDIA, Microsoft, Meta Platforms and Imbue has been a major growth driver. Dell Technologies’ shareholder-friendly approach makes it an attractive investment.

Dell is a prominent PC maker and is expected to benefit from recovering demand driven by the PC-refresh cycle. It has earlier noted that 300 million PCs will turn four years old next year, most of which are notebooks. The increasing adoption of remote working is expected to benefit the PC refresh cycle. AI-enabled architectures from Intel and Advanced Micro Devices, as well as Windows on Arm, are expected to help drive demand in calendar years 2024 and 2025. This bodes well for Dell Technologies’ Client Solutions Group segment, which contributed 55% to fiscal 2024 total revenues.

DELL sports a Zacks Rank #1 and has a Growth Score of A. The Zacks Consensus Estimate for fiscal 2025 earnings has been revised upward by 3 cents to $7.82 per share in the past seven days, which suggests a 9.7% year-over-year increase. The long-term earnings growth expectation for the company is 11.8%.

Dell Technologies Inc. Price and Consensus

Dell Technologies Inc. price-consensus-chart | Dell Technologies Inc. Quote

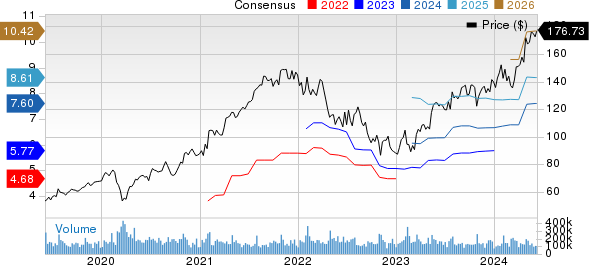

Alphabet’s robust cloud division is aiding substantial revenue growth. Expanding data centers, cloud regions and availability zones will continue to bolster its presence in the cloud space. Major search updates and the removal of bad ads to enhance the search results continue to boost traffic on the company’s search engine.

Growing momentum across Google’s mobile search is contributing further. Strengthening generative AI capabilities should aid business growth in the long term. Deepening focus on the wearables category remains a tailwind. Expanding presence in the autonomous driving space is a plus.

The Zacks Consensus Estimate for 2024 earnings has been revised upward by 3 cents to $7.60 per share in the past 30 days, which suggests year-over-year growth of 31%. This Zacks Rank #1 stock has a Growth Score of B and has an estimated long-term earnings growth rate of 17.5%.

Alphabet Inc. Price and Consensus

Alphabet Inc. price-consensus-chart | Alphabet Inc. Quote

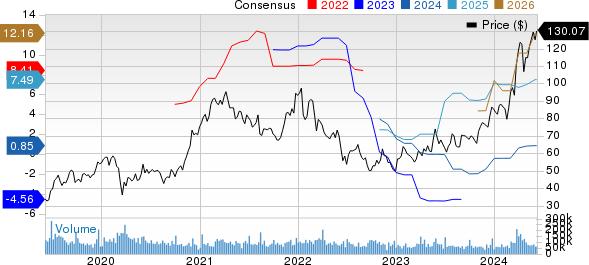

Micron has been on a recovery path from the financial difficulties experienced in late 2022 and early 2023. This improvement is evident from the company's financial results in the last few quarters. Micron is benefiting from improved market conditions, robust sales executions and strong growth across multiple business units. The positive impact of inventory improvement in the data center, as well as stabilization in other markets, such as automotive, industrial and others, is contributing to top-line growth.

Micron anticipates the pricing of DRAM and NAND chips to increase next year, thereby improving its revenues. The pricing benefits will primarily be driven by rising AI servers, causing a scarcity in the availability of cutting-edge DRAM and NAND supply. Also, 5G adoption in the Internet of Things devices and wireless infrastructure is likely to spur demand for memory and storage.

Currently, Micron carries a Zacks Rank #2 and has a Growth Score of B. The Zacks Consensus Estimate for fiscal 2024 earnings has moved 5 cents north in 30 days to 85 cents per share, which indicates a robust improvement from fiscal 2023’s loss of $4.45 per share. For fiscal 2025, the consensus mark suggests that earnings will jump approximately ninefold to $7.49 per share.

Micron Technology, Inc. Price and Consensus

Micron Technology, Inc. price-consensus-chart | Micron Technology, Inc. Quote

Want the latest recommendations from Zacks Investment Research? Today, you can download 7 Best Stocks for the Next 30 Days. Click to get this free report

Dell Technologies Inc. (DELL) : Free Stock Analysis Report

Micron Technology, Inc. (MU) : Free Stock Analysis Report

NVIDIA Corporation (NVDA) : Free Stock Analysis Report

Alphabet Inc. (GOOGL) : Free Stock Analysis Report