Adobe (ADBE) Q2 Earnings & Revenues Beat Estimates, Rise Y/Y

Adobe Inc. ADBE released second-quarter fiscal 2024 non-GAAP earnings of $4.48 per share, beating the Zacks Consensus Estimate by 2.05%. The figure improved 14.6% on a year-over-year basis.

Total revenues were $5.31 billion, which beat the Zacks Consensus Estimate of $5.28 billion. The figure rose 10% on a reported basis and 11% on a constant-currency basis from the year-ago quarter.

Top-line growth was driven by the strong performances of Adobe Creative Cloud, Document Cloud and Experience Cloud. Accelerating subscription revenues also contributed well.

Growing generative artificial intelligence efforts contributed well.

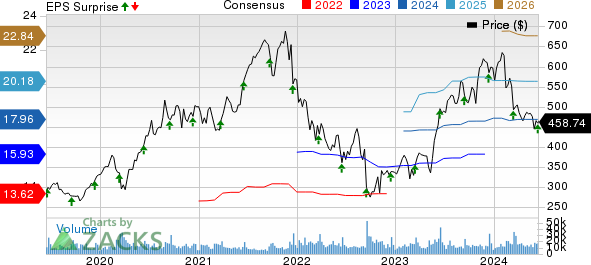

Adobe Inc. Price, Consensus and EPS Surprise

Adobe Inc. price-consensus-eps-surprise-chart | Adobe Inc. Quote

Top Line in Detail

Adobe reports revenues under three categories — subscription, product, and services & support.

Subscription revenues were $5.06 billion (accounting for 95.3% of the total revenues), up 12% on a year-over-year basis.

Product revenues totaled $104 million (2% of the total revenues), down 20% year over year.

Services & other revenues were $145 million (2.7% of the total revenues), decreasing 14.2% from the prior-year quarter.

Segmental Details

Digital Media: The segment generated revenues of $3.91 billion, which improved 11% on a year-over-year basis. The figure surpassed the Zacks Consensus Estimate of $3.79 billion. The segment comprises Creative Cloud and Document Cloud. Digital Media’s annualized recurring revenues (“ARR”) increased to $16.25 billion, of which the net new ARR was $487 million.

Creative Cloud generated $3.13 billion in revenues, up 10% year over year. The figure beat the Zacks Consensus Estimate of $3.06 billion. Creative ARR was $13.11 billion. The company witnessed the solid adoption of Creative Cloud All Apps across various geographies and customer categories, which contributed well to subscription growth. Strength in single apps, including imaging, photography and design, along with Adobe Stock, was a positive. The growing traction across Express mobile and Express for Business was a plus. The strong adoption of Firefly-powered tools drove the segment’s performance. Growing momentum across small and medium businesses (SMBs) on the back of Team offering contributed well.

Document Cloud’s revenues were $782 million, up 19% from the prior-year quarter. The figure surpassed the consensus mark of $726 million. Document cloud ARR was $3.15 billion. Solid momentum across the Acrobat ecosystem was a positive. Rising Acrobat subscription demand across various customer segments and geographies contributed well. Strength in Acrobat Web, owing to positive contributions from Microsoft Edge and Google Chrome integrations, which boosted free-to-paid conversions, was a positive. Also, growing Teams subscription unit sales to SMBs drove top-line growth.

Digital Experience: The segment generated revenues of $1.33 billion, up 9% on a year-over-year basis and beating the consensus mark of $1.28 billion. Experience Cloud subscription revenues were $1.20 billion, rising 13% from the year-ago quarter. Strength across transformational accounts, and Data Insights & Audiences and Customer Journey categories drove subscription revenue growth. Strong demand for AEP and native apps contributed well. The solid adoption of AEM and Workfront solutions was another positive.

Operating Details

The gross margin was 88.7%, which expanded 60 basis points (bps) on a year-over-year basis.

Adobe incurred operating expenses of $2.83 billion, reflecting a 7.9% year-over-year increase. As a percentage of the total revenues, the figure contracted 120 bps to 53.2% from the year-ago quarter.

The adjusted operating margin was 47.6%, expanding 60 bps year over year.

Balance Sheet & Cash Flow

As of May 31, 2024, the cash and short-term investment balance was $8.1 billion, up from $6.8 billion as of Mar 1, 2024. Trade receivables were $1.6 billion, down from $2.1 billion in first-quarter fiscal 2024.

Long-term debt was $4.13 billion at the end of second-quarter fiscal 2024 compared with $2.14 billion at the end of first-quarter fiscal 2024.

Cash generated from operations was $1.94 billion in the reported quarter versus $1.2 billion in the previous quarter. Further, the company repurchased 4.6 million shares in the fiscal second quarter.

Guidance

For third-quarter fiscal 2024, Adobe projects total revenues between $5.33 billion and $5.38 billion. The Zacks Consensus Estimate for the same is pegged at $5.39 billion.

Adobe expects Digital Media revenues between $3.95 billion and $3.98 billion. The Digital Experience segment’s revenues are expected between $1.325 billion and $1.345 billion.

Net new ARR in the Digital Media segment is projected to be $460 million. Subscription revenues of Digital Experience are anticipated to be $1.20-$1.22 billion.

Management expects non-GAAP earnings per share between $4.50 and $4.55. The consensus mark for the same is pinned at $4.46.

For fiscal 2024, Adobe projects total revenues between $21.4 billion and $21.5 billion. The Zacks Consensus Estimate for the same is pegged at $21.42 billion.

Adobe expects Digital Media revenues between $15.80 billion and $15.85 billion. The Digital Experience segment’s revenues are expected between $5.325 billion and $5.375 billion.

Net new ARR in the Digital Media segment is projected to be $1.95 billion. Subscription revenues of Digital Experience are anticipated to be $4.775-$4.825 billion.

Management expects non-GAAP earnings per share between $18.00 and $18.20. The consensus mark for the same is pinned at $17.96.

Zacks Rank & Stocks to Consider

Currently, Adobe carries a Zacks Rank #3 (Hold).

Some better-ranked stocks in the broader technology sector are Arista Networks ANET, Badger Meter BMI and Dropbox DBX, each sporting a Zacks Rank #1 (Strong Buy) at present. You can see the complete list of today’s Zacks #1 Rank stocks here.

Arista Networks’ shares have gained 30.6% in the year-to-date period. The long-term earnings growth rate for ANET is anticipated to be 15.68%.

Badger Meter’s shares have gained 27% in the year-to-date period. The long-term earnings growth rate for BMI is projected at 15.57%.

Shares of Dropbox have declined 22.6% in the year-to-date period. The long-term earnings growth rate for DBX is expected to be 11.44%

Want the latest recommendations from Zacks Investment Research? Today, you can download 7 Best Stocks for the Next 30 Days. Click to get this free report

Badger Meter, Inc. (BMI) : Free Stock Analysis Report

Adobe Inc. (ADBE) : Free Stock Analysis Report

Arista Networks, Inc. (ANET) : Free Stock Analysis Report

Dropbox, Inc. (DBX) : Free Stock Analysis Report